Meta Stock (NASDAQ:META): AI Spending Spree, Record Profits, and the $1,000 Price Target – Is It Still a Buy?

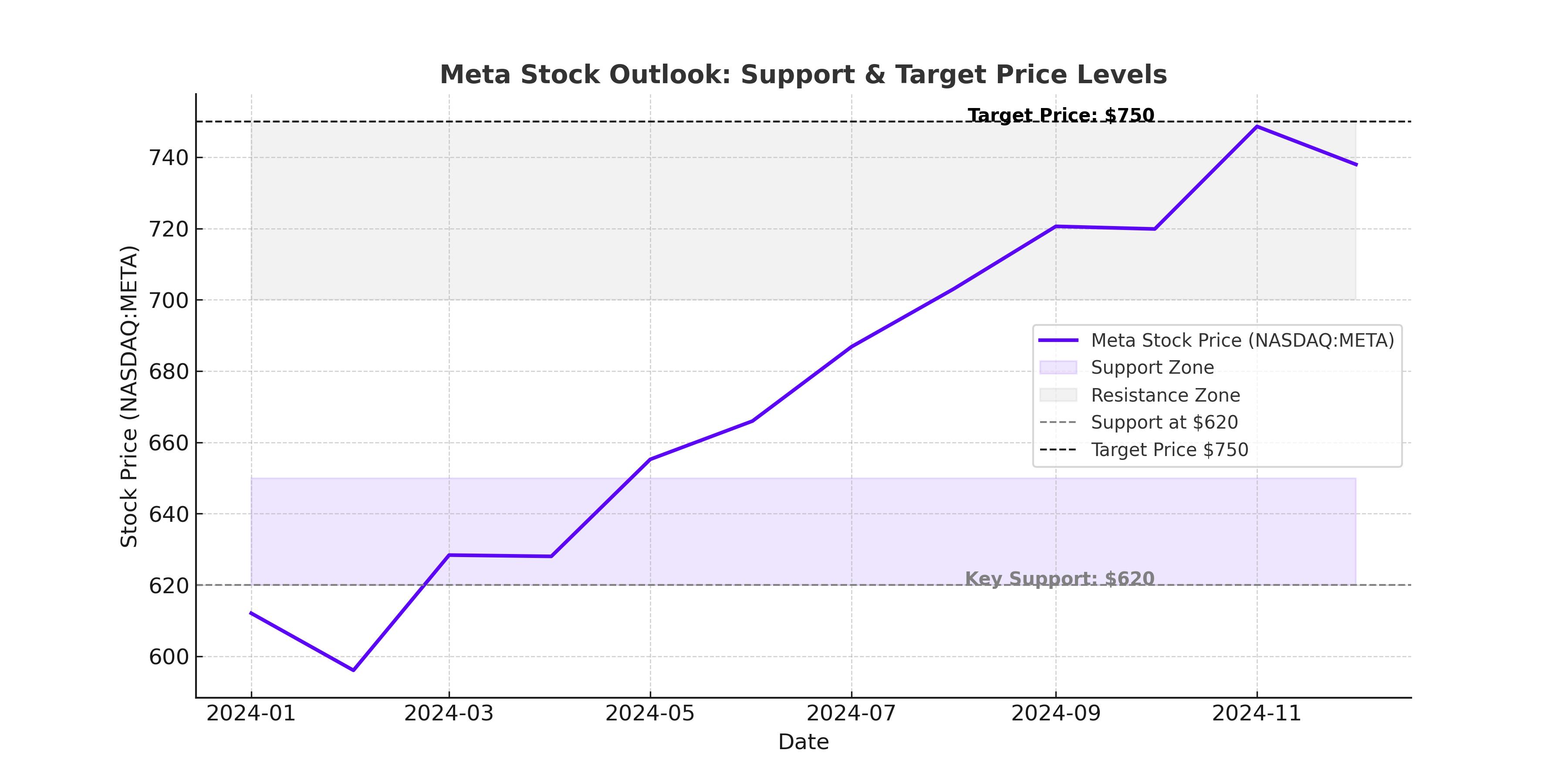

Meta Platforms (NASDAQ:META) has been on an absolute tear, soaring 49% year-to-date and climbing an astounding 675% since November 2022, when the stock crashed below $100. Investors who stuck with Meta through its rough patch have been rewarded beyond expectations, but after a six-day losing streak, questions are emerging: Is Meta still a buy, or is the company spending too much on AI and infrastructure?

Meta’s latest financials paint a picture of unprecedented profitability, but concerns are mounting over its $60-$65 billion capital expenditure (CapEx) budget for 2025. While the company’s advertising business remains dominant, its push into artificial intelligence (AI), wearables, and the metaverse is costing billions. The real question is: Can Meta’s AI investments fuel long-term growth, or are they burning cash with no clear returns?

Meta (NASDAQ:META) Stock Performance – Skyrocketing, but Cooling Off?

Following its Q4 earnings report, Meta stock went on a historic 20-day winning streak, pushing the price to record highs near $700. Even after the recent pullback, shares are still just 8% off their all-time high, reflecting confidence in the company’s business model and future prospects.

Yet, with a market capitalization of $1.7 trillion, many investors are asking whether Meta’s price-to-earnings (P/E) ratio of 27.7x forward earnings is still justified. The stock’s 15-year average P/E is 31.4x, meaning it’s technically undervalued compared to historical levels, but as growth slows, can it maintain these valuations?

Meta’s AI Ad Domination – The Secret to Soaring Profits

Meta has mastered the art of monetizing AI in digital advertising, leveraging its vast user base across Facebook, Instagram, Messenger, and WhatsApp to dominate the space. The company reported 21% year-over-year revenue growth, reaching $48.4 billion in Q4, driven by:

- 6% growth in ad impressions

- 14% growth in average price per ad

These numbers are staggering for a company this size. More impressively, Meta’s operating margin surged to 48%, a 700-basis-point expansion from the previous year. This is where Meta is outpacing Alphabet (NASDAQ:GOOGL)—while Google’s ad business is diversified across search, YouTube, and cloud services, Meta’s AI-powered recommendation system is proving more effective in engagement and ad conversion.

Meta has also reduced its workforce by nearly 30% since 2023, cutting expenses while maintaining revenue growth. The result? A 50% increase in earnings per share (EPS), which hit $8.02 per share in Q4, blowing past analyst estimates of $6.77 per share.

The $65 Billion Question – Is Meta Spending Too Much on AI?

While AI has supercharged Meta’s advertising business, its $60-$65 billion planned CapEx for 2025 has some investors worried. This massive investment—focused largely on AI infrastructure—dwarfs what was initially expected.

For context:

- Microsoft (NASDAQ:MSFT) is planning to spend $80 billion on AI in 2025

- Alphabet (NASDAQ:GOOGL) is allocating $75 billion

- Amazon (NASDAQ:AMZN) is also in the $70 billion range

While AI is critical to future growth, how much is too much? Will this level of spending deliver enough revenue to justify the cost? Meta claims that AI-powered ad optimization and custom AI chips will reduce costs over time, but 2025’s budget still raises red flags.

WhatsApp Monetization – The Untapped Goldmine

While Meta’s advertising business is booming, its potential to monetize WhatsApp remains one of its biggest opportunities. WhatsApp currently has 2.5 billion users, yet its annual revenue is estimated at just $2 billion. That’s nothing compared to the potential scale of monetization efforts.

Potential revenue streams from WhatsApp include:

- Business API & Ads: Already gaining traction, expected to bring in billions over time.

- WhatsApp Pay: If WhatsApp captures just $100 billion in total payment volume (TPV) and charges a 1% fee, it would generate $1 billion in revenue. If that scales to $500 billion in TPV, Meta could see $5-10 billion in new revenue.

- Subscription Model: If just 5% of users (125 million people) subscribed to a premium version of WhatsApp at $2.99/month, Meta would rake in an additional $3.5 billion per year.

With these revenue streams combined, WhatsApp could generate more than $10 billion annually by 2027, giving Meta a huge new growth driver outside of traditional advertising.

AI, VR, and Wearables – The Next Big Bets

Meta’s AI investments extend beyond ads. The company is heavily focused on AI-powered assistants, custom AI chips, and next-generation virtual reality (VR) and augmented reality (AR) devices.

- Meta AI Assistant: Aiming to reach over 1 billion users

- Custom AI Chips: Designed to replace reliance on NVIDIA (NASDAQ:NVDA) GPUs and lower operational costs

- Ray-Ban Meta AI Glasses & Quest VR: Targeting the next evolution of computing

If these bets pay off, Meta could become the leader in AI-powered consumer hardware, creating new high-margin revenue streams.

Meta’s Valuation – How High Can It Go?

After its six-day decline, Meta is trading at a 27.7x forward P/E, below its 15-year average of 31.4x. Analysts project EPS growth of 33.28% through 2027, bringing its forward P/E down to 20.67x by then.

For comparison:

- Amazon (NASDAQ:AMZN) trades at 31.38x 2027 earnings

- Microsoft (NASDAQ:MSFT) trades at 30.5x

- Alphabet (NASDAQ:GOOGL) trades at 27.2x

If Meta continues delivering double-digit revenue growth and expanding profit margins, a $1,000 stock price by 2027 is realistic.

Risks – What Could Go Wrong?

Meta is in a strong position, but risks remain:

- Regulatory Issues: Governments are cracking down on Big Tech’s data practices, AI dominance, and market control.

- AI Spending Risks: If Meta’s AI investments fail to generate significant returns, profitability could suffer.

- Competition: Amazon, Google, and Netflix (NASDAQ:NFLX) are ramping up digital ad spending, challenging Meta’s dominance.

- Cybersecurity Threats: As a data giant, Meta is a prime target for cyberattacks.

Final Take – Buy, Sell, or Hold NASDAQ:META?

Meta’s AI-powered ad business is thriving, its profit margins are expanding, and WhatsApp monetization offers a multi-billion-dollar opportunity. Despite its massive $65 billion AI spending spree, the stock remains undervalued compared to other Big Tech giants.

After a six-day losing streak, the recent pullback presents a buying opportunity. If AI spending delivers the expected revenue growth, Meta could reach $1,000 per share within the next two years.

Verdict: BUY NASDAQ:META with a $900-$1,000 price target by 2027.