Netflix Stock (NASDAQ:NFLX) Is on Fire – Will It Break $1,500?

With NFLX at $1,043 and climbing, is now the time to buy before it skyrockets? | That's TradingNEWS

Netflix (NASDAQ:NFLX): The $1,500 Question—Can It Keep Dominating the Streaming War?

Netflix (NASDAQ:NFLX) has completely transformed itself from a growth-first, cash-burning machine into a highly profitable, cash-generating powerhouse. The company has shifted from a relentless focus on subscriber growth to prioritizing efficiency, operating margins, and free cash flow. Investors who still see Netflix as the same company from a few years ago are missing the real story—this is no longer a business that needs to raise prices every quarter or pour billions into unchecked content spending just to stay ahead. Netflix is now one of the most financially disciplined companies in the media industry, and the numbers prove it.

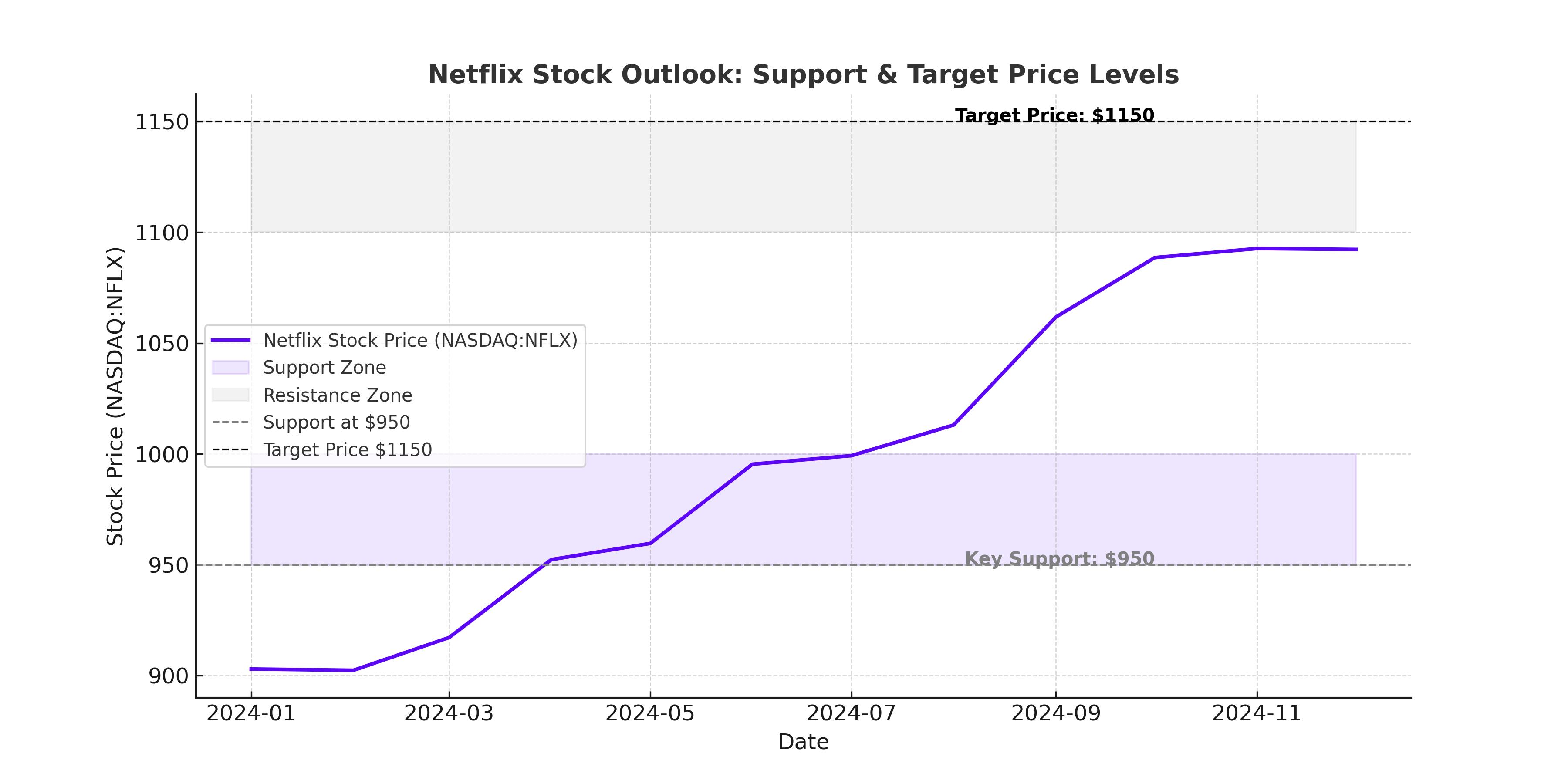

Shares of NASDAQ:NFLX have been on fire, trading at $1,043 per share, and the stock still has plenty of room to run. Over the next 12–18 months, a move toward $1,500 per share is entirely possible as more investors come to terms with how much stronger Netflix’s financials have become.

Netflix’s Financial Strength – The Market Is Still Underestimating It

Netflix isn’t just growing its subscriber base—it’s making more money per user while controlling costs. This is a business that’s now generating $7.36 billion in operating cash flow and sitting on $9.58 billion in cash and short-term investments. Instead of using all that capital to fund new content, Netflix is returning money to shareholders through stock buybacks, with $6.2 billion worth of buybacks in 2024 alone.

If a company is aggressively repurchasing its own stock, that tells you one thing: management believes it’s undervalued.

Operating income has surged 50% year-over-year, hitting $10.41 billion, while net income skyrocketed 61% to $8.71 billion. That’s a massive increase in profitability at a time when other streaming services are still bleeding cash.

Subscriber growth is still solid, with a 27% increase in Asia-Pacific and a 16% rise in Latin America, but the real story is in the improving efficiency of the business. The company’s operating margin expanded from 21% to 27%, meaning Netflix is keeping more of every dollar earned. That’s a sign of a company that has learned how to scale profitably—something that even Disney+ (NYSE:DIS) and Amazon Prime (NASDAQ:AMZN) have struggled to replicate.

Why the Stock Still Has Room to Run

At first glance, Netflix’s valuation might seem stretched, with a P/E ratio of 28x 2026E EV/EBITDA. But that doesn’t tell the whole story. This is a business that’s growing earnings at an accelerating pace, improving margins, and generating cash flow at record levels.

Revenue for 2024 hit $39 billion, a 16% year-over-year increase, but what’s more important is how efficiently the company is operating. Netflix used to spend recklessly on content, often overpaying for licensing deals and greenlighting expensive productions that didn’t deliver strong returns. That’s no longer the case.

The company’s $16.2 billion content budget is now laser-focused on maximizing engagement and retention, with an emphasis on franchises, international hits, and a mix of licensed and original content. About 90% of content expenses are recognized within four years, meaning Netflix isn’t weighed down by old, expensive shows that no longer generate revenue.

This shift from “spend to grow” to “focus on profits” is a fundamental change that the market still hasn’t fully priced in.

Netflix’s debt remains steady at $13.8 billion, with interest expenses climbing to $718 million, but with the company generating billions in free cash flow, debt isn’t a concern. Unlike in previous years, Netflix is no longer reliant on borrowing to fund its operations.

Ad-Supported Streaming – The Game Changer No One Saw Coming

Netflix’s ad-supported tier is growing faster than expected, and Wall Street is underestimating its potential. In Q4 2024, 55% of new sign-ups opted for the ad tier, up from 50% in Q3. This is a huge deal because Netflix is no longer just relying on subscription fees for revenue—it’s now making money from advertising as well.

The company’s management has set a goal of doubling ad revenue, and given the rapid adoption of the ad-supported plan, that goal looks more than achievable. Netflix’s ad platform still isn’t as mature as YouTube’s (NASDAQ:GOOGL) or Hulu’s, but it’s improving rapidly. If Netflix can prove to advertisers that their platform drives real engagement and conversions, ad revenue could become a multi-billion-dollar business on its own.

The Competition Is Tough, but Netflix Still Has an Edge

Netflix remains the king of streaming, but the competition is heating up. Disney+ is still losing money, Amazon Prime is bundling streaming with e-commerce, and Apple TV+ (NASDAQ:AAPL) is throwing billions into high-quality content.

The biggest risk for Netflix isn’t just competition—it’s piracy and changing viewer habits. More people are turning to illegal streaming sites as the cost of legal subscriptions rises. If piracy continues to grow, Netflix could lose a significant amount of revenue that it will never get back.

There’s also the challenge of keeping people engaged. The company isn’t just competing against other streaming services—it’s competing against YouTube, TikTok, and even video games. If Netflix doesn’t keep delivering hit content, subscriber churn could rise, forcing the company to spend more on marketing and retention.

International Growth – The Biggest Long-Term Opportunity

Netflix’s strongest growth is coming from international markets, but it’s a double-edged sword. The Asia-Pacific region saw a 27% increase in subscribers, while Latin America grew by 16%, but average revenue per user (ARPU) dropped 5% in both regions.

This means Netflix is adding millions of users, but at lower price points. That’s not necessarily a bad thing—Netflix’s strategy is to get users in the door with cheaper plans and gradually increase monetization through ad-supported tiers and premium upgrades.

The real challenge for Netflix in international markets is government regulations. Some countries require a certain percentage of content to be locally produced, forcing Netflix to invest in shows and movies that may not travel well to other markets. Currency fluctuations are also a problem—Netflix lost $1.42 billion in revenue in 2024 alone due to foreign exchange rate changes.

Still, the global expansion story is intact. The company is betting big on local-language content, and if it can successfully grow ARPU in these markets over time, international subscribers will become a massive profit center.

The $1,500 Price Target – How Realistic Is It?

Right now, Netflix trades at $1,043 per share, and analysts are starting to revise their price targets upward. A move to $1,500 in the next 12-18 months is entirely possible if:

- Ad revenue continues to grow at a rapid pace

- Subscriber growth remains strong, particularly in international markets

- The company keeps expanding operating margins

Netflix is no longer just a streaming company—it’s a dominant media and advertising powerhouse. If the company executes its plan effectively, a $1,500 stock price is within reach.

Final Verdict – Buy, Sell, or Hold?

Netflix is no longer a high-risk, high-reward streaming gamble—it’s a profitable, cash-flow-generating machine. The stock remains undervalued given the company’s strong earnings growth, expanding margins, and growing ad business.

With record profits, aggressive stock buybacks, and untapped ad revenue potential, Netflix remains a strong buy, with a price target of $1,500+ by late 2025. The market still hasn’t fully priced in how much stronger this company has become—and investors who wait too long might miss the next big move.

That's TradingNEWS

Read More

-

QQQ ETF At $626: AI-Heavy Nasdaq-100 Faces CPI And Yield Shock Test

11.01.2026 · TradingNEWS ArchiveStocks

-

Bitcoin ETF Flows Flip Red: $681M Weekly Outflows as BTC-USD Stalls Near $90K

11.01.2026 · TradingNEWS ArchiveCrypto

-

Natural Gas Price Forecast - NG=F Near $3.33: NG=F Sinks as Supply Surges and China Cools LNG Demand

11.01.2026 · TradingNEWS ArchiveCommodities

-

USD/JPY Price Forecast - Dollar Breaks Toward ¥158 as Yen Outflows and US Data Fuel Dollar Charge

11.01.2026 · TradingNEWS ArchiveForex